Is Mobile Money industry having a “Nokia moment”?

Given the trend in smartphone adoption in Africa and the growth of Fintech challengers, mobile money operators are facing a changing market and customer behaviour. Being too slow to react and adapt may be fatal.

I started my Fintech career by joining M-Pesa in 2011 and spent some of the most inspiring entrepreneurial years of my professional life there, working in Kenya, Tanzania but also leading its expansion into new markets like Egypt, Romania and more. Since then, M-Pesa experienced some tremendous growth and “mobile money” became an industry, banking hundreds of millions of people worldwide. In 2024, M-Pesa’s transaction volume alone exceeded $100 billion, compared to $120bn Kenya GDP the same year. Mobile money became the backbone of many economies in Africa, and with average transaction value being $10.99 in Kenya (less in other African markets), its role in including the low-income population in the financial system is unparalleled so far.

Last summer, I was in China and had a chance to contrast the mobile money industry with the evolution of Ant Financial, or what is called today The Ant Group. Ant Financial’s consumer-facing brand AliPay started with similar use cases of p2p and bill payments and moved quickly to enable the 2010s e-commerce revolution in China. However, it never stopped there. The Ant Group has today evolved into a life-encompassing super app, allowing its customers to shop, move, access credit, mortgages, get financial advice, insurance and more.

This visit only emphasized for me what has been obvious for a while; mobile money industry needs to “disrupt itself” by moving away from USSD and cash out revenues at agents to app-based services and complex financial services offerings.

Key trends requiring Mobile Money disruption

Today, majority ofmobile money users still use the USSD and SMS channels which in 2024 accounted for over 70% [1] of mobile money transactions processed in Sub-Saharan Africa compared to over 90% in 2018 [2]. While most operators have launched smartphone apps, the GSMA, industry body, reports app penetration among the customer basefor many MOMOs is below 10%.

At the same time, fuelled by cheaper devices from China and India, the smartphone penetration among African populations is growing faster than the mobile money smartphone usage. As of 2024, smartphone ownership in Sub-Saharan Africa stood at 36% and is projected to rise to over 50% by 2028 [3]. This trend points to a) an opportunity for the smartphone customers to be acquired by alternative Fintech apps and b) the threat of MMOs missing out on its customer base’s changing behaviours, risking having them slip way to fintech players.

The innovation in financial service industry in Africa continues, and the number of potential competitors is growing, fuelled by the venture capital industry. Since 2018, the number of venture capital funds and corporate investors in Africa has grown from 155 in 2018 [4] to 615 in 2024 [5]. And while the VC funding has dropped since its peak of $6bn being invested in African Startups in 2022, today we witness a stable and active venture capital industry with $2.6bn raised in 2024 across more than 500 deals. Of this funding, more than 50% went to the Fintech sector [6].

The risk of customers slipping away from Mobile Money Operators is also illustrated by the “verticalization” trend among young smartphone users. Namely, while mobile money may still be the mostly used service for p2p transfers, and airtime purchases, the reports show that young Kenyans use 3-5 different financial apps for their different financial needs: saving, loans or insurance. The ability offintechs to “specialize” in one use case, perfect it and provide the best service on that front is a real threat to “generalist” mobile money operators, who happen to also be large companies, typically innovating much slower due to their size, governance and internal processes.

The case of Wave

Wave launched in 2008 as a spin-off from Sendwave, essentially pursuing an uber-aggressive strategy vs local money transfer operators in Senegal, i.e., MTN and Tigo - freshly acquired by Axian Group. Riding a wave of easy capital spilling into Africa, Wave decided to subsidize its growth by waiving consumer fees on cash in and cash out - essentially killing the main revenue stream for MMOs – cash out fees. Itis important to note that the Wave breakthrough to a leader in Senegal with between 4 and 5 million active users, representing around 90% of the adult population holding a Wave account [7], should be considered a case of real disruption and an early warning to MOMOs, due to:

· Its channel disruption, aimed at disrupting the hegemony of Telcos by providing its services through app only [8]. This was a bold move as smartphone penetration was still in low teens, but it broke the dependence on USSD and SMS and improved the user experience.

· Its aggressive pricing strategy of 0 fees for cash out, while still paying commissions to agents, was only possible in the time of cheap capital flows, as its growth was subsidized with VC equity investments.

Since the “Profitability Era” for African Fintech started in 2023, Wave has gone throughthe needed restructuring, made its org and ops leaner, and managed to raise additional VC equity ($200 million Series A round led by Sequoia Heritage, Founders Fund, Stripe, and Ribbit Capital) and debt financing ($137million round in July 2025 led by Rand Merchant Bank with BII, Norfund, and Finnfund) [9].

MOMO’s Nokia moment. Ecosystem Play is the Future

While the times of hot VC funding, which initially helped create Wave, are over, African VC industry is here to stay. With forecasted $3bn invested in 2025, 100+ fintechs being funded each year, innovating and building solutions that customers, SMEs and financial players themselves need. They move fast, test fast, fail fast and adapt fast tobuild tech solutions and user-friendly smartphone apps that customers are willing to use and pay for. On the other hand, Mobile Money Operators are large organizations, still heavily relying on a SMS and USSD technologies and legacy technology infrastructure that is slowing down their innovation potential.

This reality painfully reminds us of Nokia’s market situation in 2000s. The world class manufacturer of mobile phones in the 1990s, at certain point holding a staggering 30% globalmarket share, was facing competition from Apple, Google and Samsung smartphones, and consumer behaviour shift from feature phones, voice and SMS to smartphone apps usage. Nokia was slow to react and build its own smartphone, and when it finally did, it underestimated the need to build a developer-friendly strategy and grow its own ecosystem of applications. This eventually resulted in its mobile phone business shutting down.

So, how can MOMOs avoid Nokia’s fate? Is partnering with startups an opportunity not to be missed?

At @First CircleCapital, we believe the African Fintech ecosystem is reaching a maturity where ecosystem play, partnerships and embedded finance are the winning strategies for sustainable growth. This is exacerbated by slower deployment of VC Capital and Fintech industry pursuing a profitability mantra. Mobile Money Operators will benefit from partnering with agile, developer-led startups creating new products, services and software that can improve the way they operate and serve their customers. On the other hand, the fintech startups will be keen to work with incumbent operators with large customer base, reducing their cost ofcustomer acquisition. We believe it’s not too late for MOMOs to rebuild their position in markets like Senegal and Ivory Coast and retain their role by leveraging partnerships and pursuing a broader ecosystem play.

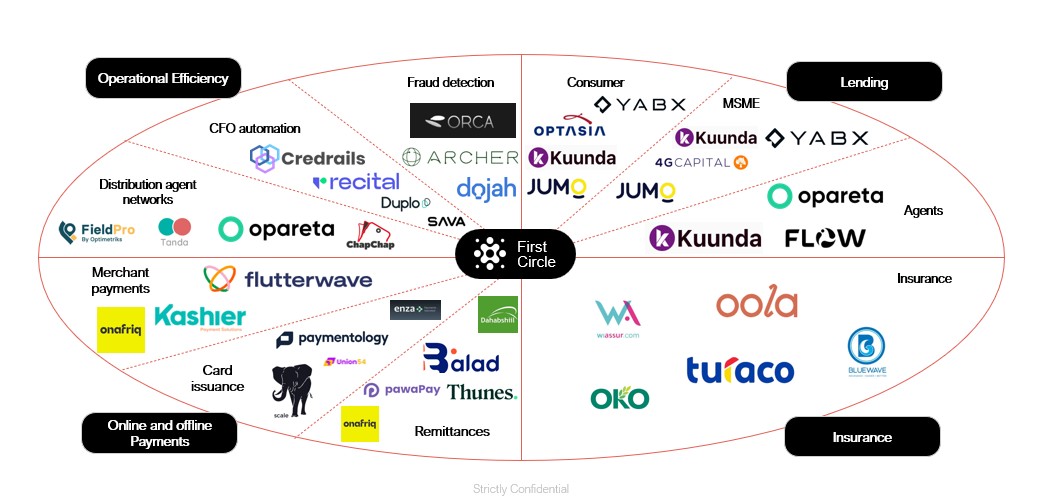

The market map attached to this article illustrates different areas of key partnership opportunities for Mobile Money Operators with two key goals:

· Improve operational efficiencies. We expect this area to become more important asthey spin off Fintech from Telecom businesses, and move to raise externalcapital for growth.

· Product Extension: Partners with whom they can launch new products for their customer base, such as Lending, Insurance or Merchant Payments. This requires continued effort to place MOMMO rails at the centre of each market’s fintech ecosystem and it will have substantial effect on increasing ARPU per MOMO user and increased stickiness of their consumer base.

We are bullish about the future of financial services in Africa, driven by partnerships and embedded finance.

Sources:

[1] https://hsenidmobile.com/why-telcos-in-africa-still-rely-on-ussd-gateways-in-2025/

[2] GSMA- State of the Industry Report on Mobile Money 2018

[3] https://dataxis.com/researches-highlights/1633344/rising-affordability-will-push-smartphone-access-to-half-of-africas-population-by-2028/

[4] Disrupt Africa - The African Tech Startups Funding Report 2021

[5] AVCA- Venture Capital in Africa Report 2024

[6] Africa: The Big Deal / Startups Deals Database– December 2024 Update

[7] https://tropicsmag.com/venture-spotlight-wave-the-senegalese-fintech-unicorn-revolutionizing-mobile-money-in-africa/

[8] https://www.wave.com/en/blog/early-execution/

[9] https://techpoint.africa/insight/techpoint-digest-1126/